Despite Being Significantly Cheaper, Mortgage Loans Struggle to Sell

Households had taken out free-use mortgage loans totaling little more than 11 billion forints by the end of February, with the number of new contracts failing to reach even 750.

This is despite the product being significantly cheaper than personal loans.

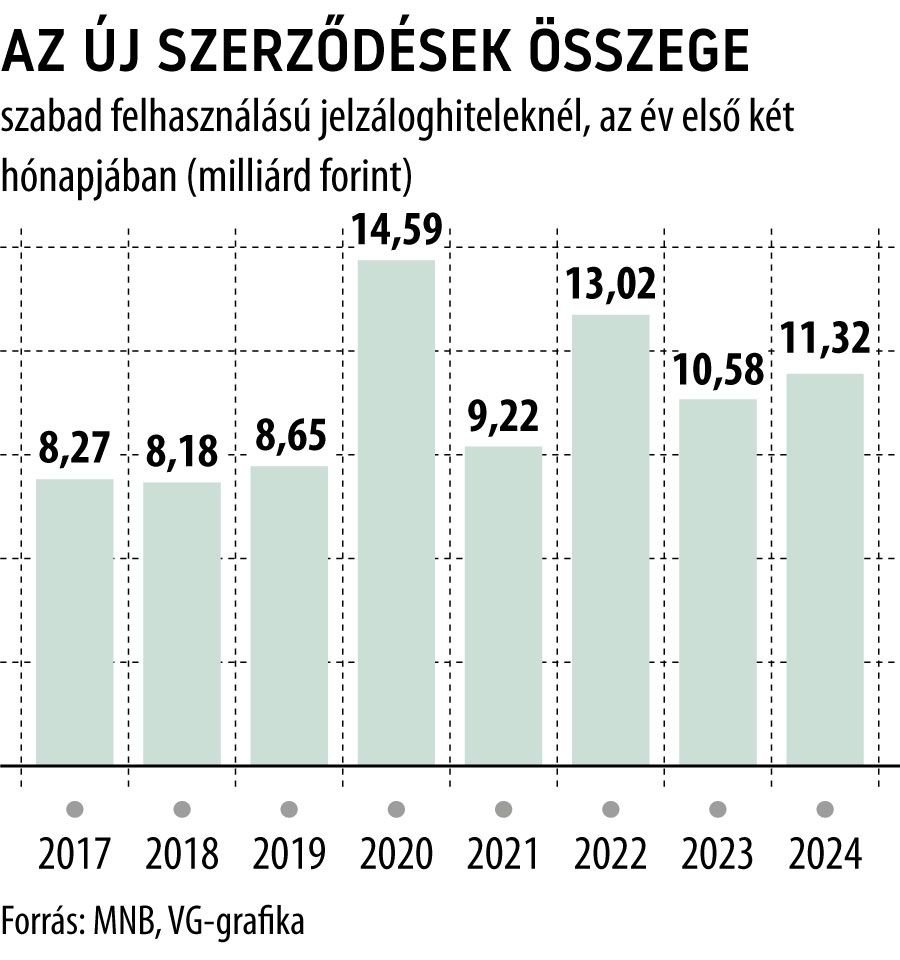

The free-use mortgage loan market showed a rather modest performance in the first two months of the year: the value of new contracts reached 11.3 billion forints, only 7 percent higher than the 10.6 billion a year earlier, according to data from the Hungarian National Bank (MNB). Although a 7 percent increase might not seem bad in itself, given the performance of the entire retail credit market in the first two months of this year, it is not considered exceptional.

Meanwhile, the number of new mortgage loan contracts increased from 659 to 741 in an annual comparison, which resulted in the average amount per contract decreasing from around 16 million forints to 15.3 million.

However, last year was not unfavourable for free-use mortgage loans: according to MNB data, customers signed new contracts totalling 90.9 billion forints, nearly 13 percent more than the year before. This was achieved despite 2023 being rather gloomy for the retail credit market. However, a one-time effect was needed to achieve the steady double-digit growth: the introduction of government securities with favorable interest rates led many to start taking loans for speculative purposes, aiming to profit from the interest rate differential, which for months was well reflected in the mortgage loan disbursements.

The overall subdued demand for mortgage loans is naturally reflecting on stock data as well: according to the central bank's data, by the end of February, the mortgage loan portfolio had shrunk to around 726 billion forints, which is 2.3 percent less than a year earlier, albeit only slightly.

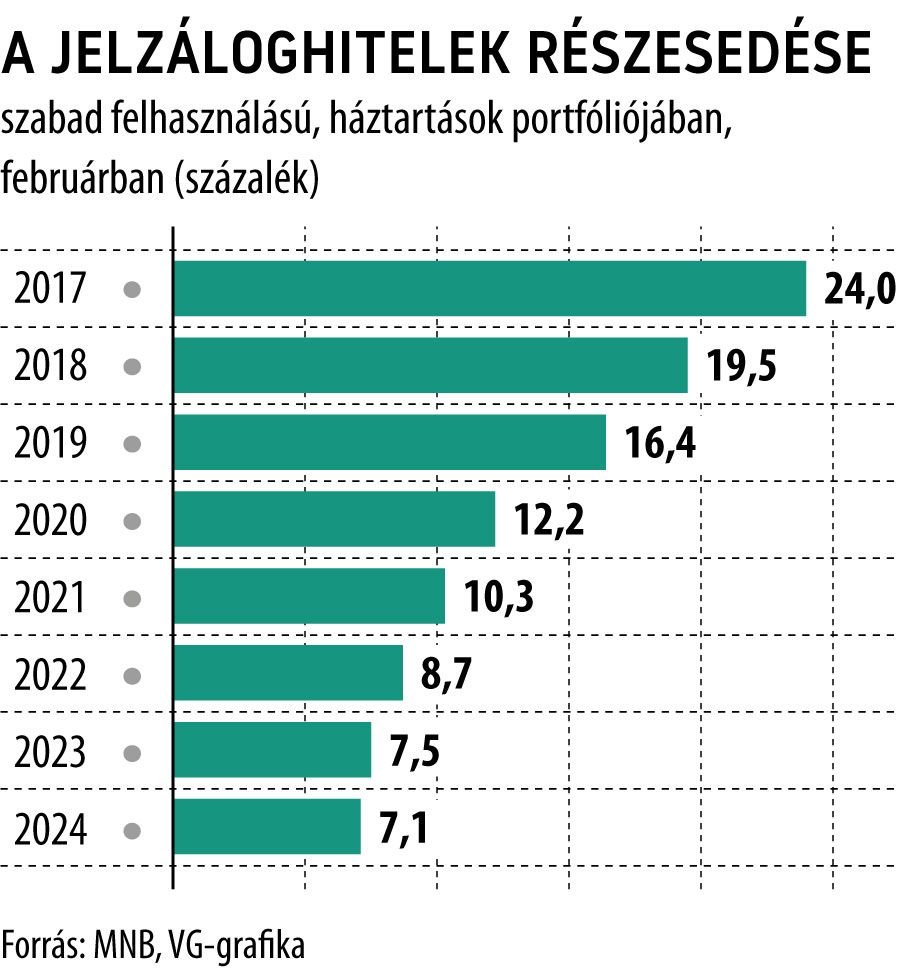

Mortgage loans now barely exceed 7 percent of the total retail portfolio, while three years ago, their weight was well over 10 percent.

The modest demand can clearly be explained by the advances in personal loans. Although mortgage loan interest rates in February were approximately 9 percent lower compared to the latter at an average annual value of 9.56 percent the much easier and faster access pushes the majority of those planning to take out loans towards personal loans.

This might also be contributed to by the significant increase in the maximum available loan amount for personal loans in recent years, and the option for entirely online applications is now available at several financial institutions, with same-day disbursement. In contrast, applying for free-use mortgage loans still involves weeks of administrative time and extra costs, not to mention that the borrower must offer a lien-free property as collateral.

The free-use mortgage loan market showed a rather modest performance in the first two months of the year: the value of new contracts reached 11.3 billion forints, only 7 percent higher than the 10.6 billion a year earlier, according to data from the Hungarian National Bank (MNB). Although a 7 percent increase might not seem bad in itself, given the performance of the entire retail credit market in the first two months of this year, it is not considered exceptional.

Meanwhile, the number of new mortgage loan contracts increased from 659 to 741 in an annual comparison, which resulted in the average amount per contract decreasing from around 16 million forints to 15.3 million.

However, last year was not unfavourable for free-use mortgage loans: according to MNB data, customers signed new contracts totalling 90.9 billion forints, nearly 13 percent more than the year before. This was achieved despite 2023 being rather gloomy for the retail credit market. However, a one-time effect was needed to achieve the steady double-digit growth: the introduction of government securities with favorable interest rates led many to start taking loans for speculative purposes, aiming to profit from the interest rate differential, which for months was well reflected in the mortgage loan disbursements.

The overall subdued demand for mortgage loans is naturally reflecting on stock data as well: according to the central bank's data, by the end of February, the mortgage loan portfolio had shrunk to around 726 billion forints, which is 2.3 percent less than a year earlier, albeit only slightly.

Mortgage loans now barely exceed 7 percent of the total retail portfolio, while three years ago, their weight was well over 10 percent.

The modest demand can clearly be explained by the advances in personal loans. Although mortgage loan interest rates in February were approximately 9 percent lower compared to the latter at an average annual value of 9.56 percent the much easier and faster access pushes the majority of those planning to take out loans towards personal loans.

This might also be contributed to by the significant increase in the maximum available loan amount for personal loans in recent years, and the option for entirely online applications is now available at several financial institutions, with same-day disbursement. In contrast, applying for free-use mortgage loans still involves weeks of administrative time and extra costs, not to mention that the borrower must offer a lien-free property as collateral.

Translation:

Translated by AI